Digital Banks vs. Traditional Banks: Why Mobile Banking Experience Is Becoming the New Trust Factor

Digital banks have increased mobile engagement rates by nearly 50% annually—not because of bigger budgets, but because of three interconnected capabilities. AI is now accelerating the speed at which those capabilities compound.

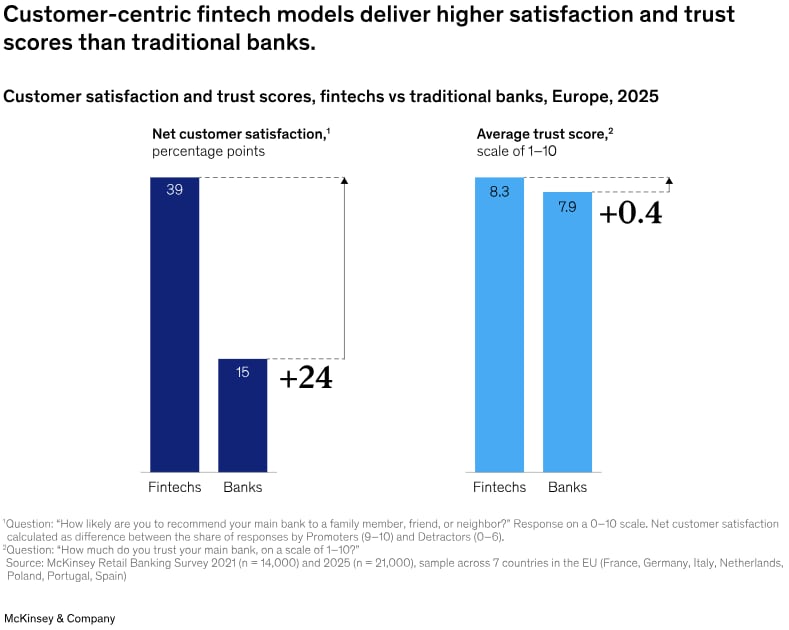

The starkest view of the competitive shift comes from McKinsey's Global Banking Annual Review (May 2026): not only are fintechs and neobanks delivering greater satisfaction, but they’re also now leading on banking customer trust—the one thing traditional banks assumed was permanently theirs.

Both sides have real advantages. Both sides also have serious blind spots.

Digital Banks: What They Built, and What It’s Costing Them

The three capabilities driving the gap:

- Behavioral segmentation: Targeting actions like "viewed loan calculator 3 times" outperforms demographic targeting by 3–5X.

- Deep linking: Eliminates 50–70% of conversion loss between a campaign tap and the in-app destination.

- Connected measurement: Ties every touchpoint to a real outcome: funded accounts, loan applications, and deposits—not clicks.

What’s changing now is that AI in banking is becoming the force multiplier behind all three capabilities.

Segmentation models that once took weeks to build and validate can now adapt in real time as customer behavior changes. AI can identify patterns that traditional rule-based systems often miss, allowing institutions to deliver more relevant messaging, offers, and next-best actions at the moment a customer is most likely to engage.

Measurement infrastructure is evolving as well. Instead of relying on analyst teams to manually connect performance data across channels, AI can automatically surface insights, identify attribution trends, and recommend budget reallocations based on actual business outcomes. The result is faster decision-making and more efficient marketing spend.

Perhaps most importantly, AI enables institutions to move from reactive marketing to predictive engagement. Rather than responding to what customers have already done, banks can anticipate needs, identify potential churn risks, recommend relevant products, and create personalized experiences across digital channels.

For traditional financial institutions, the opportunity is not simply to become more mobile-first. It’s to combine the trust, customer relationships, and brand equity they’ve spent decades building with AI-driven capabilities that make every customer interaction more intelligent, measurable, and relevant.

Here’s what that looks like in practice. Your bank sends a fraud alert. The customer taps it and lands on the home screen. They scroll, give up, and call support. A digital bank sends the same alert; the customer taps it and lands directly on that exact transaction—resolved in ten seconds, and no call needed. Users who engage this way show 2X higher transaction likelihood and 2.7X higher spend than customers who hit a generic home screen.

That isn’t just a UX story. It’s a retention and cost necessity. The institutions delivering the strongest mobile banking experience are increasingly the ones reducing support burdens while deepening customer engagement.

The blind spot:

The moment something breaks, digital banks have no fallback. No branch. No relationship manager. No human escalation path—and in many cases, no support infrastructure built for the market the customer is actually in.

According to the JD Power 2026 US Direct Banking Satisfaction Study, neobanks are struggling with a higher incidence of customer problems—falling short on ease of reaching customer service, resolving issues in a single contact, and delivering support that meets customers where they are.

Personalization is frictionless until it isn’t. Then there is nothing.

The fix:

Build the human layer before a trust crisis forces it. Invest in multilingual support infrastructure, real escalation paths, and customer communications that work in every market—not just the one your product team lives in. The most sophisticated digital banks operating at scale across Europe already understand this: 69 million customers across a continent means dozens of languages, regulatory regimes, and support expectations that a single-market playbook cannot cover.

The ones treating it as an afterthought are building a trust problem they’ll have to unwind later.

Traditional Banks: What They Still Own, and How Fast They’re Losing It

The real advantage:

- Millions of opted-in, first-party customer relationships with decades of behavioral data.

- FDIC-backed credibility neobanks can’t carry independently and instead rely on partnerships with traditional banks.

- Owned escalation paths. AI virtual assistants consistently fall short on complex service and fraud issues; traditional banks still own the human alternative.

The blind spot:

Traditional banks are barely using any of it. Institutions lost an average of 3.36 digital applications for every successful account opened—a figure that barely moved year over year. Some of that friction is technical. Some of it is language: onboarding flows built in English and never adapted for the customers trying to complete them.

Fintechs' share of combined revenues among the largest 1,000 banks and top 1,000 fintechs rose from 10% in 2021 to 17% in 2025.

The fix:

Three things. None require replacing core systems. AI is the connective tissue running across all of them.

- Move beyond demographic segmentation.

Traditional segmentation tells you who a customer is. AI-powered behavioral segmentation tells you what they’re likely to do next. Institutions can identify customers who are ready to convert, at risk of attrition, primed for cross-sell opportunities, or engaging with content but not taking action. It also helps uncover underserved customer segments, including those who may be more responsive when engaged in their preferred language.

- Eliminate friction between campaign and conversion.

Deep linking ensures customers arrive at the exact screen, product, or action they intended to access. AI strengthens this process by determining which message, channel, offer, and timing are most likely to drive engagement. The goal isn’t simply more traffic—it’s fewer abandoned journeys and higher conversion rates.

- Measure what drives outcomes, not just activity.

Mobile banking adoption continues to rise, generating an enormous volume of customer behavior data every day. Statistics show that 82% of mobile banking users were active in 2025, up from 73% in 2024. As institutions compete for engagement, retention, and long-term customer value, improving the mobile banking experience has become a strategic priority. Yet many institutions still struggle to connect that activity to meaningful business outcomes. AI-powered measurement platforms can identify which channels influence account openings, loan applications, deposits, and customer retention, allowing teams to allocate resources based on impact rather than assumptions.

That’s daily behavioral data sitting unmeasured inside most traditional institutions. AI turns that data into action. Most banks are still turning it into reports.

The Trust Factor—and Why It Changes Everything

Customers' attitudes are reaching a tipping point. They not only favor but increasingly trust the new entrants delivering reliable everyday services. The trust advantage was supposed to be permanent. It isn’t. And digital banks still haven’t solved the human support problem that could hand that advantage back to traditional institutions.

The battle for banking customer trust increasingly comes down to execution: delivering seamless digital experiences while providing reliable human support when customers need it most.

The real question isn’t whether traditional banks can become more mobile-first. It’s whether they will use AI in banking to combine the execution speed of a challenger with the trust and relationships of an institution that has served customers for decades.

Neobanks like Revolut are scaling execution across dozens of languages and markets. Traditional institutions like JPMorgan Chase are also investing in AI-driven infrastructure to match that speed—saving billions and boosting versatility without sacrificing the credibility they already own. Both are moving.

Those who close their gap first will take the market. Those who don’t will spend the next decade explaining why they had every advantage and still lost the customer.

The window is open now. See what action looks like: https://www.transperfect.com/financial